By Brendan Wagner, Senior Wealth Manager

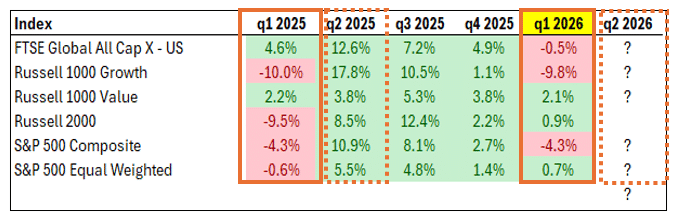

Stock market returns in Q1 2026 were remarkably similar to the year-ago returns of Q1 2025. In both quarters, large growth fell and large value rose. In subsequent months last year, large growth stocks then recovered strongly after a similar decline. Whether that happens again is part of our discussion.

As noted in the table below, this past quarter saw a rotation out of the biggest companies into midsize and small in addition to value.

(Source: http://www.ftserussell.com/, http://www.djindexes.com/)

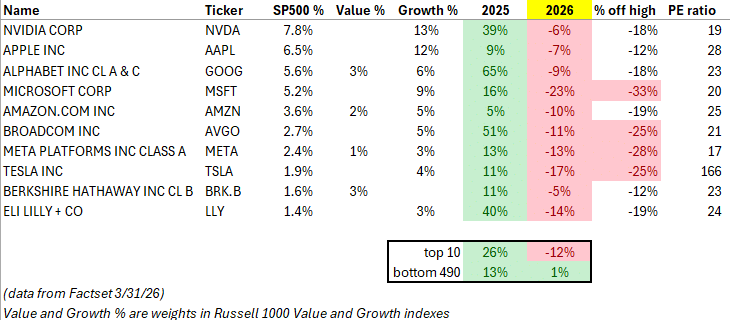

The ten largest stocks in the S&P500 Index (below) beat “the rest” by 13 percentage points in calendar year 2025 and are lagging by the same degree through Q1 2026. These biggest companies account for 38% of the S&P500 Index weight, 9% of the Russell 1000 Value Index, and a whopping 59% of the Russell 1000 Growth Index.

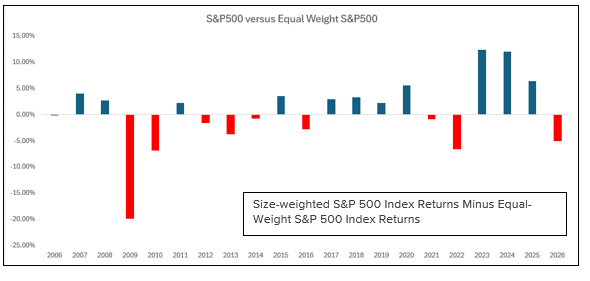

Considering the “Large” in “Large Growth” may help explain the recent relative weakness in the market’s ten largest stocks and why this rotation from biggest into everything else has occurred. The law of large numbers suggests companies like Microsoft or Nvidia, whose market capitalizations exceed $2.5 trillion, may be hard-pressed to continue to grow earnings at the rapid pace of the last few years. Historically, investors are wary of paying high P/E ratios for companies where the earnings upside is tougher to achieve. Many active investors appear to be reconsidering what appropriate valuation levels ought to be for behemoth companies well past their entrepreneurial years – and reevaluating what weight these companies deserve in their portfolios. Only in recent years (2023-2025) has it become “normal” for the size-weighted S&P500 to continuously trounce the average stock, as seen below. It may continue to become less normal going forward.

Earlier in the first quarter, a series of essays and blog posts regarding artificial intelligence spooked investors. Reactions were swift and pronounced in software and industries such as consulting, data, and info providers, types of businesses conspicuously highlighted as ones at risk of replacement by large language models (LLMs). While near-term earnings expectations for these companies have not changed for the most part, investors expressed their concern by assigning lower valuations: when P prices fall more than E earnings, the result is lower P/E ratios. Reduced valuations reflect an uptick in perceived risks to their long-term future growth potential. It is also important to consider the source of growth one is paying for when owning a stock. Is it growth in the number of customers, the number of products/services purchased by existing customers, or higher prices paid by existing customers? Some forms of growth may be less valuable than others.

Another component at work may be an underlying and potentially ongoing shift in the investor base, where growth/momentum focused-investors appear to have fled certain stocks in droves while potential growth-at-a-reasonable-price buyers, with different approaches to investing, were not ready to plunge in with fresh purchases. This perspective also offers a partial explanation of the rotation out of growthier sectors into stocks with lower valuations early in the quarter.

Time out of the market is historically the biggest drag on long-term returns. Thoughtful asset allocation aligned with an understanding of one’s risk tolerance and capacity are vital to preserving and growing wealth. Spencer Jakab of the WSJ once used a great term – “Fortune Favors the Unconscious,” to describe the benefits of doing nothing in fast moving, often chaotic declining stock markets. “Doing something” usually involves selling, and by the time this fear reaches one’s psyche, it may be too late to be productively proactive. While we cannot control near-term market volatility, or other investors’ priorities, we can do our best to position thoughtfully ahead of time and respond calmly.

A year ago, individuals, business owners, and economists alike worked hard to absorb and incorporate announcements of new US tariff policies into their expectations for the future. Policy announcements were made or revised unexpectedly, and stock markets fluctuated as rapidly as the headlines. With the benefit of hindsight, it is easy to recognize that, in the moment of surprise, more negative outcomes seemed possible at the time than those which actually occurred. In other words, most of the time, the worst-case scenario does not materialize. For this reason, the stock market nearly always troughs and reverses higher well before definitive resolutions are clear.

Returning to the present day: the closure of the Hormuz Strait has injected large “air pockets” into what before had been routinely available supplies of energy components, chemicals, fertilizers, helium, and other basic materials. The full scope of this impact is still unfolding. Southeast Asian countries are particularly reliant on Middle East oil, and some locations are instituting “energy lockdown” policies.

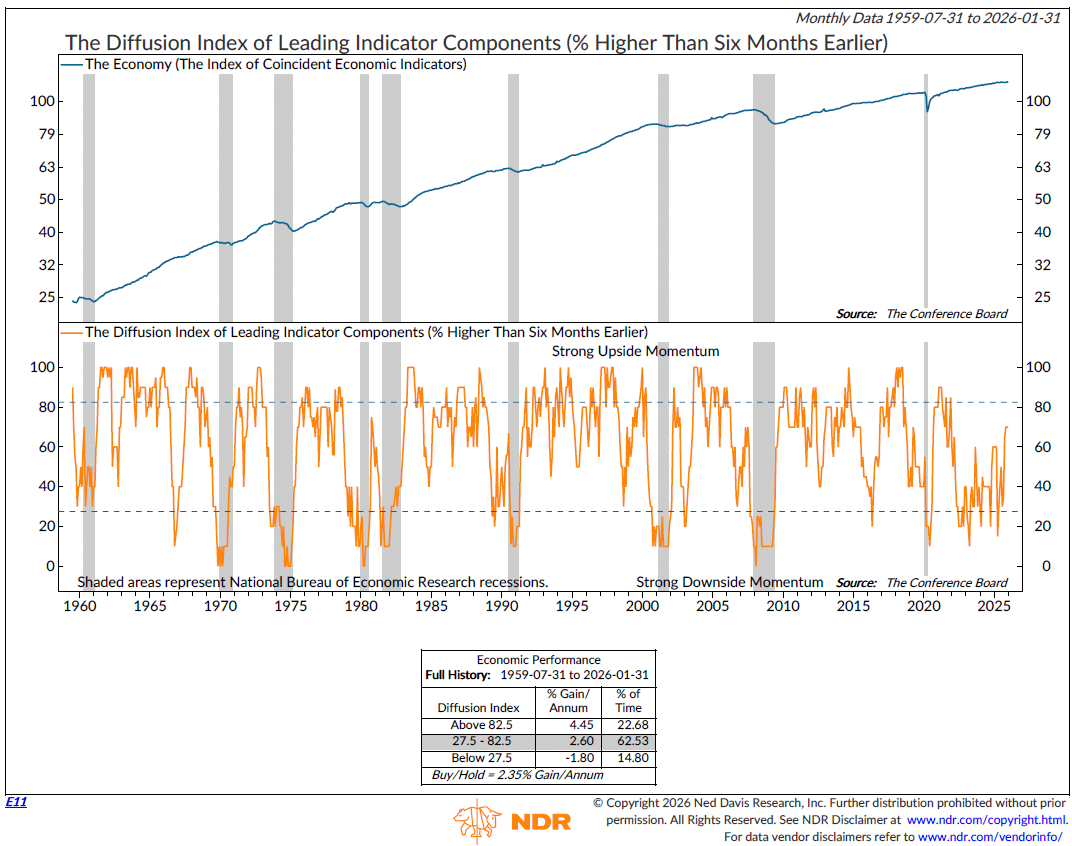

In the US, we expect explicit and implicit fuel surcharges to be added to many goods and services, and it remains to be seen how these and other hot-war-related expenses will be distributed. Fortunately, the economy was demonstrating positive forward momentum prior to this conflict. As seen below, as of late January 2026, the ISM’s Diffusion Index of Leading Indicator Components (the percentage of indicators higher than six months earlier) was the broadest in four years, at 70%:

(Source: Ned Davis Research, 3-31-2026)

In our view, equities remain richly valued compared to history, compared to bonds offering nearly mid-single digit entry yields. Amidst turmoil, keep in mind that the companies making up our client portfolios (as well as the large indexes) have weathered wars and recessions and other headwinds in the past, and underestimating their ability to weather current storms is unwise.

Disclosure:

The information provided is for illustration purposes only. It is not, and should not, be regarded as “investment advice” or as a “recommendation” regarding a course of action to be taken. These analyses have been produced using data provided by third parties and/or public sources. While the information is believed to be reliable, its accuracy cannot be guaranteed. MONTAG employees do not provide legal or tax advice. For specific legal or tax matters, you should consult with your own legal and/or tax advisors. There are risks associated with investing in securities. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Loss of principal is possible.