By Christine R. Quillian, CFA, CFP®, Senior Wealth Manager

The second quarter of 2026 produced the strongest S&P 500 gain since 2020, up 14.9% after a 4.3% first-quarter decline. What began with geopolitical stress, oil volatility, and tariff uncertainty ended with many indexes near record highs, supported by signs of broadening leadership and a powerful earnings recovery across major size and style segments.

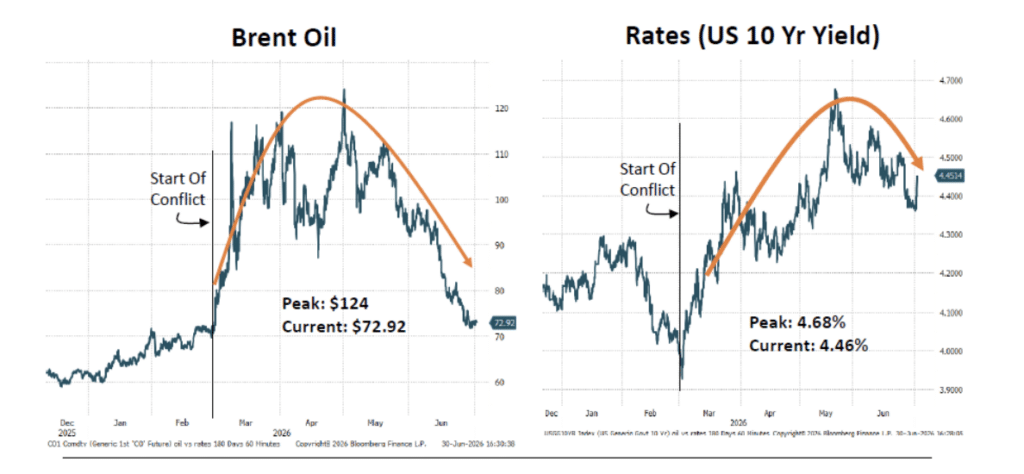

Oil and rates defined the quarter’s turning points. Oil spiked sharply to $124 per barrel before retreating to the low $70s, while the 10-year Treasury yield rose from 4.32% to a mid-May peak near 4.66% before easing. By quarter-end, simultaneous relief in energy and rates helped reduce inflation anxiety and supported risk assets.

Piper Sandler 7-1-2026

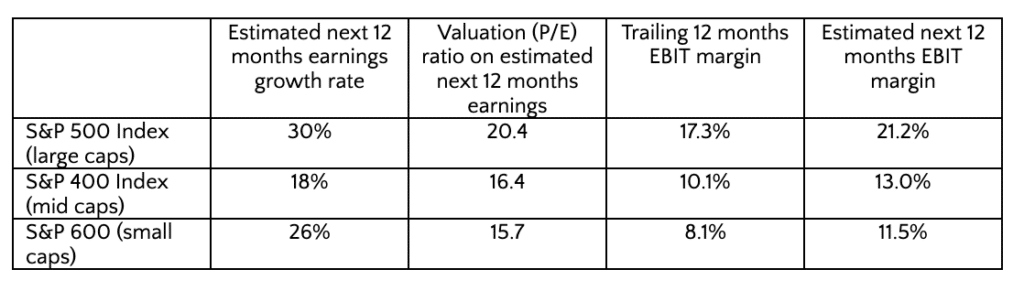

The first half included several incongruous pairings. Gold weakened despite geopolitical tensions; usually it benefits from war risk, inflation angst and safe-haven demand. Instead, gold sold off as the stronger USD and higher rate expectations overwhelmed the geopolitical bid. On an absolute basis, 9 of 11 sectors are up year-to-date and small caps outperformed despite higher interest rates. Most importantly, fundamentals—not multiple expansion—drove returns: forward S&P 500 earnings estimates rose roughly 18%–19% since January while valuation multiples compressed.

The second-half outlook still appears to favors equities, but with a bumpier path. After 10%-plus up quarters, markets have historically been higher six months later 85% of the time, yet only one 5% pullback so far this year suggests limited cushion. Sticky inflation, fading expectations for near-term Fed cuts, midterm election year seasonality, and widening dispersion across AI beneficiaries and credit quality warrant a more selective approach.

Second-Quarter Recovery: April Through June

A Record-Setting Rebound

The recovery from the March 30 low was decisive. Every US size and style segment advanced in Q2, led by small-cap growth at 23.4%. Large-cap value was up “only” 7.5% – still excellent for any three month period. 30% of S&P 500 Index constituents reached all-time highs at some point during the quarter.

The late-June easing of US-Iran tensions helped reverse the oil shock. Oil retreated to roughly $70 as supply fears eased, OPEC+ raised supply, China reduced crude imports, and flows bypassed the Strait of Hormuz. The decline in oil and Treasury yields became the main macro catalyst for new market highs.

Earnings: The Engine, Not the Multiple

The rally was also grounded in corporate fundamentals. First-quarter earnings season was exceptional, with 84% of S&P 500 companies beating estimates. Looking ahead, forward EPS growth expectations are strong across the board and valuations appropriately reflect relative differences in those growth rates and margins.

Piper Sandler 6-30-2026

Notably, earnings growth more than offset multiple compression: the cap-weighted index’s forward P/E is down roughly 8% year-to-date while EPS estimates are up roughly 18%–19%. Global PMIs also improved, with 80% now in expansion territory, suggesting economic support for corporate profits is broadening even as AI remains a growth engine.

Sector and Factor Leadership: The AI Trade Evolves

At the sector level, relative performance in Q2 was defined by sharp whipsaws and shifting leadership. After a weak Q1, technology rebounded strongly, driven by outsized gains in electronic components and semiconductor related industries. In contrast, Energy went from the best performing sector in Q1 to worst in Q2. At the deeper industry level, relative returns are proving to be highly concentrated. Of the S&P Index’s 72 industry segments, only 23 are up more than 10% for the year, and 28 (39% of all industries) are flat to down. Improvement in earnings may be broadening, but investors’ willingness to pay higher valuation multiples has not yet followed through to the same degree.

IPOs and the AI Capital Cycle

The AI capital cycle also accelerated with Space Exploration Technologies, Space-X, debuting as a public company in mid-June. Other major AI-related companies also moved toward public markets or raised large private rounds, and expected 2026 US IPO proceeds have risen sharply. The scale of capital mobilized for AI infrastructure remains a defining feature of this cycle.

Macro Backdrop: Growth, Inflation, and Policy

Growth Intact, Consumer Bifurcated

Real GDP growth in the low 2% range appears achievable in the second half, supported by AI-related capital spending, steady employment, and tax incentives. The much faster EPS growth reflects sector concentration, margin recovery, and operating leverage rather than broad GDP acceleration. The labor market seems steady, and lower energy prices should provide some relief to lower- and middle-income households, though consumers sentiment remains bifurcated by income.

Inflation: Sticky Above 3%

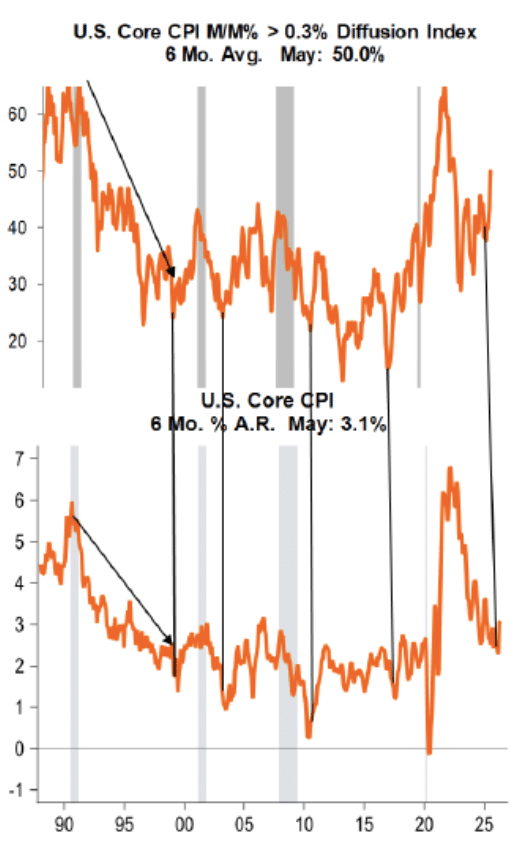

Stubborn inflation remains a constraint. Core CPI diffusion indexes show the breadth of prices increasing more than 0.3% month-to-month has been rising, now more than 50% of the components. Tariffs, energy volatility, and technology-price pressures have pushed expectations away from multiple cuts by the Fed and toward renewed tighter monetary policy before year-end. Fixed income now offers better income opportunities than a few months ago, but duration should be added selectively rather than aggressively.

Piper Sandler, 6-28-2026

Outlook: Staying Invested, Staying Selective

The Case for Equities

The evidence continues to favor an equity bias. Earnings strength is broadening, recession risk remains relatively low, global PMIs are in expansion, and many stock indexes show primary trends intact. Leadership rotation within the market is constructive, and volatility should be used to add selectively rather than broadly. We of course note that risks remain and the outcome may differ from what we expect.

Risks and Positioning for the Second Half

Risks are still meaningful. The market has had only one 5% pullback year-to-date versus a historical average of three, leaving less room for negative surprises. Furthermore, even as earnings improvements broaden, earnings optimism for the core semiconductor complex looks stretched. Midterm election year seasonality, elevated margin debt, leveraged ETF activity, oil volatility, and interest-rate sensitivity could all contribute to a choppier second half.

Positioning should remain selective: maintain exposure to profitable, higher-quality companies regardless of capitalization, and continue to monitor leadership. Quality fixed income remains attractive for income at current yields.

Disclosure:

This commentary is prepared for informational purposes only and draws on research published by J.P. Morgan Asset Management, Truist Advisory Services, UBS Global Research, Piper Sandler, Ned Davis Research, Bloomberg Intelligence, and Bloomberg News. It is not, and should not be regarded as “investment advice” or as a “recommendation” regarding a course of action to be taken. These analyses have been produced using data provided by third parties and/or public sources. While the information is believed to be reliable, its accuracy cannot be guaranteed. Specific securities identified and described may or may not be held in portfolios managed by the Adviser and do not represent all of the securities purchased, sold, or recommended for advisory clients. The reader should not assume that investments in the securities identified and discussed were or will be profitable. MONTAG employees do not provide legal or tax advice. For specific legal or tax matters, you should consult with your own legal and/or tax advisors. There are risks associated with investing in securities. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Loss of principal is possible.