By HELEN DONAHUE, CFA

Rising interest rates have caused volatility in the equity markets recently. The 10-Year Treasury started the year yielding less than 1% and swiftly moved to a recent high of nearly 1.6% the last week of February. While the move higher in yields reflects good news from both the increased distribution of vaccines which will eventually allow businesses to reopen, and lawmakers working to approve additional fiscal stimulus, the sudden move up in yields spooked equity investors accustomed to near zero interest rates which has been supportive of equity valuations. It is understandable for stocks to take a breather following the remarkable returns investors have enjoyed in the midst of the global pandemic.

Rising interest rates have caused volatility in the equity markets recently. The 10-Year Treasury started the year yielding less than 1% and swiftly moved to a recent high of nearly 1.6% the last week of February. While the move higher in yields reflects good news from both the increased distribution of vaccines which will eventually allow businesses to reopen, and lawmakers working to approve additional fiscal stimulus, the sudden move up in yields spooked equity investors accustomed to near zero interest rates which has been supportive of equity valuations. It is understandable for stocks to take a breather following the remarkable returns investors have enjoyed in the midst of the global pandemic.

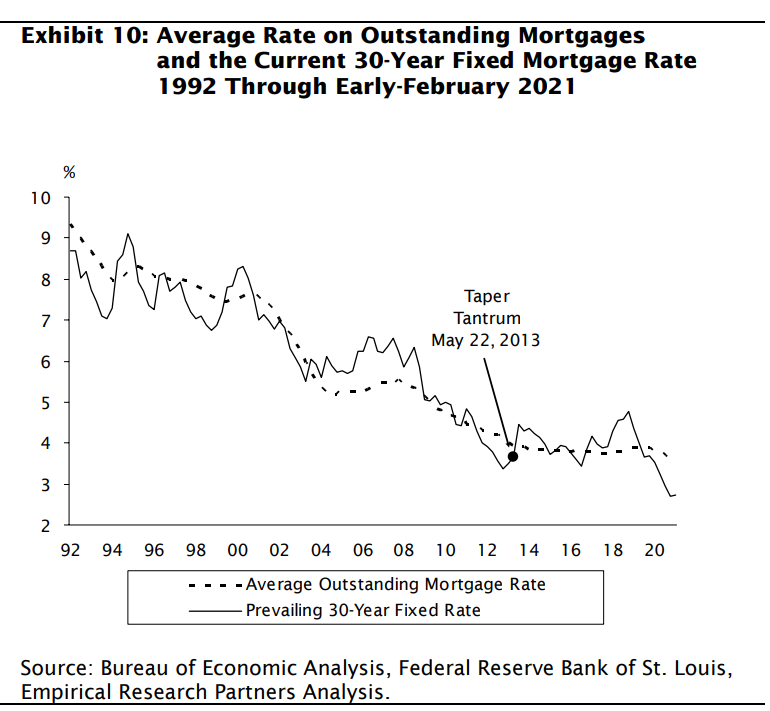

However, we continue to have a positive view on the US equity markets for a variety of reasons. First is the promise of businesses returning to normal. While select industries continue to suffer high unemployment because of the pandemic, consumers overall are flush with cash from a combination of fiscal stimulus, strong equity returns and increased savings due to a decline in travel and leisure spending. This pent-up demand should unleash spending as economies reopen. Housing demand remains strong and supply is limited, providing another pillar of support for the US economy. Despite an uptick in mortgage rates, they remain low relative to history and there is potential for continued refinancing as the average rate on outstanding mortgages is above the current rates as evidenced by the chart above.

However, we continue to have a positive view on the US equity markets for a variety of reasons. First is the promise of businesses returning to normal. While select industries continue to suffer high unemployment because of the pandemic, consumers overall are flush with cash from a combination of fiscal stimulus, strong equity returns and increased savings due to a decline in travel and leisure spending. This pent-up demand should unleash spending as economies reopen. Housing demand remains strong and supply is limited, providing another pillar of support for the US economy. Despite an uptick in mortgage rates, they remain low relative to history and there is potential for continued refinancing as the average rate on outstanding mortgages is above the current rates as evidenced by the chart above.

The Federal Reserve has not wavered in its accommodative policy stance and increases in the Federal Funds rate are a long way off since the Fed is likely to reduce its pace of bond purchases gradually first, a step they have not taken yet. While the Fed can only control short-term interest rates and longer-term yields are determined by the market, an uptick in inflation the market is expecting is likely to be short-lived due continuing productivity enhancements enabled by technology and ongoing globalization. With the exception of select industries such as leisure and hospitality, earnings for most sectors have recovered to or above pre-pandemic levels.

The Federal Reserve has not wavered in its accommodative policy stance and increases in the Federal Funds rate are a long way off since the Fed is likely to reduce its pace of bond purchases gradually first, a step they have not taken yet. While the Fed can only control short-term interest rates and longer-term yields are determined by the market, an uptick in inflation the market is expecting is likely to be short-lived due continuing productivity enhancements enabled by technology and ongoing globalization. With the exception of select industries such as leisure and hospitality, earnings for most sectors have recovered to or above pre-pandemic levels.

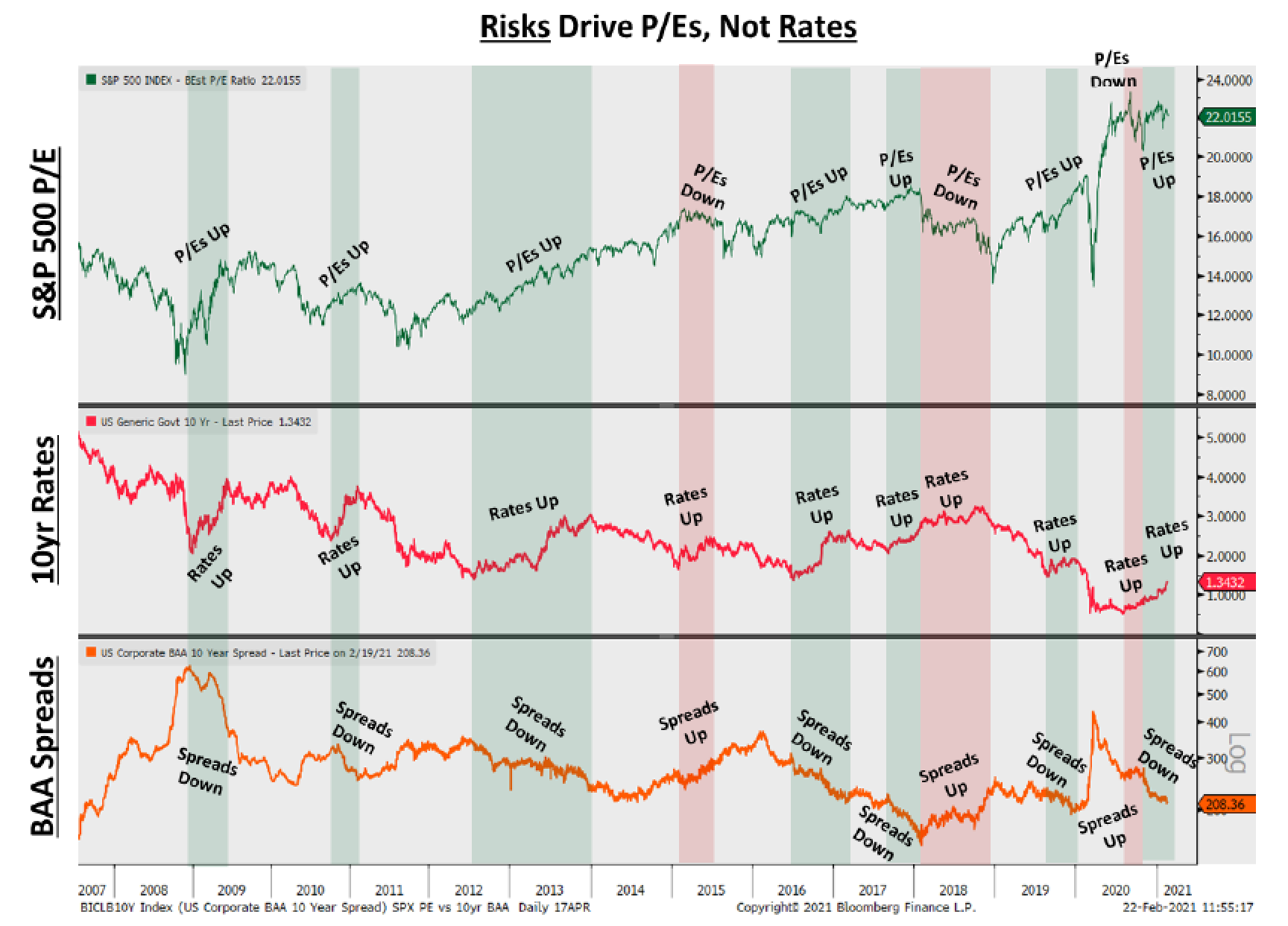

Finally, Treasury yields are not the sole driver of price to earnings multiples (P/E’s). Revenue growth, particularly in the technology sector, has been robust and earnings estimates are rising. Cornerstone Macro notes that the yield differential, or spread, on corporate bonds versus Treasury bonds is a driver of P/E multiples. Corporate bond spreads continue to compress, indicating investors remain comfortable with risk and providing support for P/E multiples.

Finally, Treasury yields are not the sole driver of price to earnings multiples (P/E’s). Revenue growth, particularly in the technology sector, has been robust and earnings estimates are rising. Cornerstone Macro notes that the yield differential, or spread, on corporate bonds versus Treasury bonds is a driver of P/E multiples. Corporate bond spreads continue to compress, indicating investors remain comfortable with risk and providing support for P/E multiples.

The information provided is for illustration purposes only. It is not, and should not be regarded as “investment advice” or as a “recommendation” regarding a course of action to be taken. These analyses have been produced using data provided by third parties and/or public sources. While the information is believed to be reliable, its accuracy cannot be guaranteed.