By Jackson Keenan, CFP® , APMA™, Director of Financial Planning

As we enter the season of giving, it is important to consider how giving can benefit both your principles and your taxes.

Many of our clients utilize Donor-Advised Funds, but they look for new charitable strategies. In this month’s blog I will dive into a few of these.

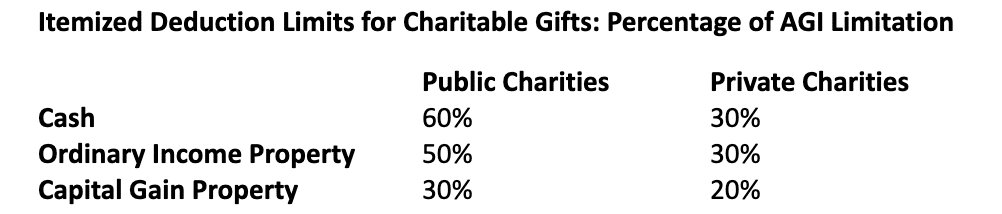

First, consider what you are giving and who it goes to impacts your taxes differently. The following chart helps explain:

To implement the above strategy, you need to itemize your taxes. Meaning your itemized deductions need to be higher than the standard deduction. (The 2025 standard deduction is $15,000 for single filers and $30,000 for married couples filing jointly. The additional deduction for those age 65 or older or blind: $2,000 if your filing status is single and $1,600 per person if married filing jointly.)

If your total itemized deductions are below these amounts you may try “donation bunching.” This is a tax strategy that consolidates your donations for two years into a single year to maximize itemized deductions for the current. This approach may produce a larger total deduction over two years than two years of standard deductions.

Next, charitable giving is also a great way to unload highly appreciated assets. Certain assets may have significantly appreciated over time and result in a substantial capital gains taxes at sale. This makes them ideal to donate and this can even be a part of a portfolio rebalance.

Finally, if you are at least age 70 ½, you should consider a Qualified Charitable Distribution (QCD). A QCD allows you to donate up to $108,000 total to one or more charities directly from a taxable IRA, tax free. This may help donors avoid being pushed into higher income tax brackets and prevent phaseouts of other tax deductions.

The 2025 donation deadline is December 31st, so the sooner you start planning the better. You can give yourself a double win: improving the world and a potential tax break too.

Citation: IRS Publication 526 Charitable Contributions and Publication 590-B (2024), Distributions from Individual Retirement Arrangements (IRAs).